Agri-Food’s Outlook in the Green Pause

From the Evergreen Investing Newsletter

This content is available thanks to subscriber support. To subscribe to the full newsletter, see subscription options here or click the button below.

Economic challenges and reactions to them are leading to a temporary slowdown in the green paradigm shift.

The clearest illustration of this is the United Nations Climate Change Conference (COP28) recently held in Dubai.

Policymakers along with energy, political, and business leaders convened to discuss and provide guidance for the world’s energy outlook. While 198 parties signed the UAE Consensus, it was one that recognized the need for countries to chart their own paths towards achieving carbon neutrality. This of course makes good practical sense, as every nation has circumstances that are specific and sometimes very different from others.

Ultimately that may slow progress toward net zero. But the reality is that elevated inflation, decelerating economies, and the risk of recession bring resistance against certain green transition initiatives, especially those with big price tags.

Food is of course critical, and high prices cause hardship. Some countries are net importers, while others are net exporters: they don’t have the same challenges or goals. So, in recognizing the importance of the agrifood sector, organizers of COP28 added a food-systems focus to their agenda. The goal is to have global governments integrate food systems and agriculture into national climate agendas, and even encourage the adoption of regenerative agriculture.

In this issue I’m going to review some of the major challenges this sector has faced, then look at what lies ahead and explain how we can benefit from addressing emerging trends.

Food Prices

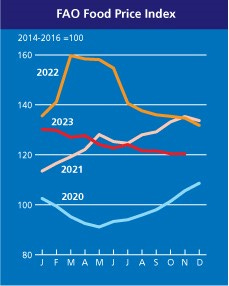

Let’s start with food prices. This FAO Food Price Index from the UN’s Food and Agriculture Organization provides a global view of food pricing over the past 60 years.

Source: Food and Agriculture Organization of the United Nations

COVID-19 wreaked major havoc from early 2020 until early 2022 by disrupting supply chains. Many countries have since aimed for self-reliance by prioritizing local food sources. These were the first major shocks.

Then came the Russia-Ukraine war launched in early 2022, triggering energy price spikes and massive grain, fertilizer, and chemical shortages. It’s clear how this caused the huge rise in food prices in the above chart from 2020 until 2023. Climate shocks in the form of droughts and disease have also been major contributors.

In response central banks embarked last year on an aggressive, coordinated cycle of raising interest rates to try and cool soaring inflation. On balance that’s provided some relief. In the US, overall inflation peaked near 9% in mid-2022 but has fallen to 3.1% lately. Meanwhile, food inflation topped at 11.4% in August last year but fell to 2.9% this past November.

Source: Food and Agriculture Organization of the United Nations

Globally, food prices have receded about eleven percent in the past year. Industry experts forecast that should continue overall into 2024.

Outlook 2024 and Beyond

According to Rabobank Research’s Agri Commodity Outlook 2024, certain subsectors are bucking the falling price trend. El Niño-related dryness has been a climate factor in 2023 that limits yields of commodities like sugar, robusta, and cocoa, especially in Southeast Asia, India, Australia, and parts of Africa.

Higher interest rates may lead to recession, helping to ease food prices. But there are counterbalancing risks. Energy and refined products prices remain elevated, and increased volatility is expected well into 2024. Some oil producers like OPEC and Russia are willing to cut production to maintain prices and exert pressure on political rivals. The Israel-Hamas war could quickly disrupt oil and natural gas supplies from the Middle East. Energy is a major input in food production and pricing.

Whether food prices rise sooner or later farmers, supply and software providers, service companies and other stakeholders will need to position themselves adequately. Animal feed and crop science company Alltech produces an annual survey: the Agri-Food Outlook. Its 2023 edition highlights that “…respondents said product prices/the economy is the consumer trend that is making the biggest impact on the agri-food industry.”

When considering technologies having the largest influence on the sector, respondents cited nutritional solutions, biosecurity, automation of labor/robotics, renewable energy technologies, IoT/smart farm applications/sensors, and data collection/analysis as the top opportunities for growth.

Source: Alltech Agri-Food Outlook 2023

So how do we as investors prepare our portfolios for the opportunities ahead?

Positioning for the Next Agrifood Boom

We need to approach these prospects from several angles. It’s possible that prices will remain subdued for a while with milder inflation. That means having exposure to solutions providers like equipment, technologies and software, beneficiaries like suppliers of livestock medicine, and leaders like environmentally conscious fertilizer producers. I think technology will have an increasingly significant role in agrifood production as farmers deal with labour shortages, intemperate climate, and gradually rising input costs.

One great example of a huge leap in this realm is John Deere’s (Deere & Co.) fully autonomous tractor. With an operator or fully automated, the 8R tractor can see and avoid obstacles with 360-degree cameras, high-speed processors, and AI to evaluate and determine if the area is safe to drive over. It even calculates exact amounts of seeds and fertilizer needed, reducing waste and environmental impact…all from the farmer’s smart phone!

Thankfully, we’ve already taken positions in two of the best ways to play the coming agri-boom.

Back in February we added the VanEck Agribusiness ETF (NYSE:MOO), which includes agribusiness companies involved in agricultural products and chemicals, animal health, fertilizers, seeds and grains, farm and irrigation equipment, aquaculture and fishing, livestock, and cultivation and plantations. MOO includes companies like Zoetis, Deere & Co., and Archer-Daniels-Midland. Zoetis is the world’s largest producer of medicine and vaccinations for pets and livestock. Deere makes equipment for farming, small agriculture and more. Archer-Daniels-Midland buys, ships, stores, processes and merchandises agricultural commodities and ingredients around the world. Each of these is a leader in its area.

Then in October I showed you how the NEW Green Revolution means meeting the demand for farm produce while using responsible fertilizers. So, we added CF Industries (NYSE:CF), the world’s largest ammonia producer (ammonia is a central ingredient of most chemical fertilizers). As CF contributes to global fertilizer production, it’s reducing its carbon footprint and advancing clean energy projects. The company has committed to reduce its total CO2 equivalent emissions by 25% per ton of product by 2030 and achieve net-zero carbon emissions by 2050. They have more than a dozen clean energy initiatives in North America, Europe, and Asia, spanning power generation, sustainable fuel, hydrogen transport and storage, low carbon ammonia for industrial applications, and a lot more.

So, as we look toward a potentially challenging 2024, we are positioned with some of the best ways to benefit from the numerous opportunities that come from adapting to changes while staying ahead of others.

This content is available thanks to subscriber support. To subscribe to the full newsletter, see subscription options here or click the button below.